Wall Street Tech Analyst: Micron Could 4x If the AI Cycle Lasts Through 2030

Wall Street Tech Analyst: Micron Could 4x If the AI Cycle Lasts Through 2030

Thomas RichmondTue, June 30, 2026 at 1:08 AM UTC

0

Canva | AndreyPopov from Getty Images and 400tmax from Getty Images SignatureQuick Read -

Luria says Micron could 4x by 2030 while Microsoft's 19x P/E looks cheap given its 50% AI compute backlog advantage over Google.

Memory faces less competition than CPUs yet Micron trades at 8-9x while CPU-leveraged names command 40-50x, a spread Luria calls illogical.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Microsoft didn't make the cut. Grab the names FREE today.

D.A. Davidson Head of Technology Research Gil Luria recently appeared on CNBC to flag what he calls a contradictory set of AI-cycle assumptions baked into chip and software valuations. His call was that if AI infrastructure spending continues to compound through the end of the decade, Micron Technology (NASDAQ:MU) could be worth roughly four times its current price. However, if the AI cycle peaks sooner instead, many of today's richly valued CPU stocks could lose a significant portion of their value.

What Gil Luria Still Sees in Micron After an 800% Run

Luria argues that memory and GPU names like Micron and Nvidia are being valued "as if the cycle is peaking now," while CPU-leveraged names such as Intel and AI-silicon challenger Cerebras are priced as if the buildout runs another five years. By his numbers, Micron is changing hands at "8 or 9 times or lower" while CPU stocks sit at "40-50 times and higher." Luria says memory is more critical to AI workloads and faces less competition than CPUs, so the spread "doesn't make any sense."

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Microsoft didn't make the cut. Grab the names FREE today.

Micron reported fiscal Q3 2026 revenue of $41.456 billion, beating consensus by 17.60%, with non-GAAP EPS of $25.11 and a GAAP gross margin of 84.6%. Cloud Memory revenue alone hit $13.769 billion. CEO Sanjay Mehrotra said the results "reflect the strategic value of memory in the AI era" and pointed to newly signed multi-year Strategic Customer Agreements designed to "significantly enhance the durability and predictability" of revenue. Management guided fiscal Q4 revenue to $50.0 billion ± $1.0 billion and non-GAAP EPS of $31.00 ± $1.00.

Micron is up 296.92% year to date and 800.86% over the past year, with a forward P/E of 7. Luria frames a potential 4x for Micron as a scenario contingent on AI spending continuing through 2030.

MU Earnings Explorer — 24/7 Wall St.

Why the Market Could Be Overlooking Microsoft

Advertisement

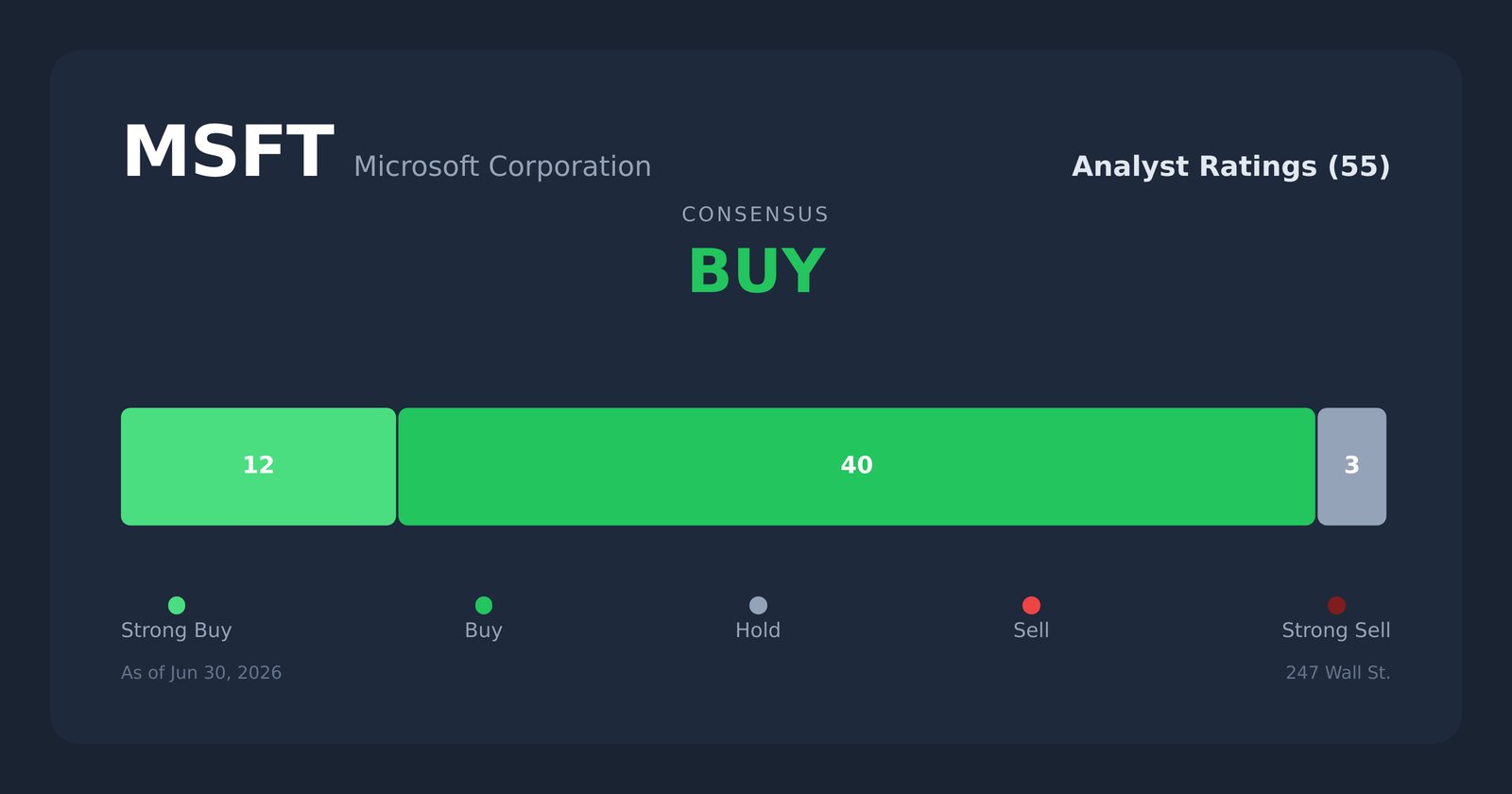

Luria's second call concerns Microsoft (NASDAQ:MSFT). He says Microsoft has "50% more AI compute backlog than Google" and is selling significant AI infrastructure software, yet is "getting punished for the same capex as Google." Luria believes the company is selling data center capacity at a meaningful markup and locking in multi-year returns, so the capex is going in at attractive economics.

Microsoft is down 22.54% year to date and 24.42% over the past year, with an 18.14% one-month decline, which Luria characterized as its worst month in a couple of decades. He notes Google traded at 18x a year ago and Microsoft at 30x, a relationship that has since inverted.

Microsoft's most recent quarter showed Azure growth of 40% year over year, an annual run rate for its AI business of $37 billion (up 123%), and commercial remaining performance obligations of $627 billion. Capex hit $30.88 billion in the quarter, the spending that flows directly into Micron's HBM and data center memory order books. Microsoft now trades at a forward P/E of 19.

MSFT Analyst Ratings — 24/7 Wall St.

What To Watch

Luria's framework centers on finding valuation disconnects, where the market is pricing a near-term AI peak for one company but years of continued growth for another. For Micron, the key question is whether its multi-year Strategic Customer Agreements and HBM4 ramp can sustain pricing power into 2027, when HBM4E is expected to enter volume production. For Microsoft, investors will be watching to see whether AI revenue growth catches up with the heavy capital spending that has weighed on sentiment. More than any single valuation multiple, Luria's thesis depends on which AI growth scenario ultimately plays out.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Microsoft didn't make the cut. Grab the names FREE today.

Contact editorial@247wallst.com for any questions or corrections.

Source: “AOL Money”